In the fast-paced world of startups, fundraising is a pivotal step that can make or break your venture. But for many busy founders embarking on their fundraising journey, the myriad of investment instruments available can be overwhelming.

Are you unsure whether to opt for a SAFE, a convertible note, or an investment agreement?

You're not alone. This article is tailored for founders like you, aiming to demystify the complexities of each option, highlighting their pros and cons. Convertible instruments, such as SAFE and convertible notes, are favored for their swift execution and cost-effectiveness, making them ideal for the early-stage rounds: pre-seed and seed. On the other hand, while investment agreements offer clarity and customization, especially for Round A+ investments, they come with their own set of challenges. Dive in to understand which tool aligns best with your startup's needs and ensure a smoother fundraising journey.

Below we’ll cover:

- Convertible instruments and how they work

- SAFEs and how they work

- Convertible notes and their key principles

- Advantages and disadvantages of using convertible instruments

- Investment agreements and what they consist of

- Key terms of investment agreements

- Advantages and disadvantages of investment agreements

Convertible instruments: what are they and how do they work?

The concept of convertible instruments is relatively new. Up until 2005-2010, all investments into companies were made by purchasing a company’s shares. At the moment where convertible instruments were introduced, the barrier to accessing venture investments was lifted and a cluster of angel investors emerged. It became obvious to many people in the industry that the old instruments (e.g. signing term sheets, shareholders’ agreements, changing company charter, etc.) were no longer effective due to the time and money spent on raising for a pre-seed round of ~$500K.

Therefore, convertible instruments were created with the most popular ones being the SAFE (the simple agreement for future equity), developed by Y Combinator, and convertible note (or convertible loan note), developed by Techstars.

What are the two key concepts of convertible instruments?

- A SAFE/convertible note investor receives shares on the next investment round (priced round). It means that when you’re issuing shares to a new investor in the next round, you should also issue shares to your previous SAFE investor(s) during the current round.

- The key task of the convertible instrument is to calculate the number of shares that the SAFE/convertible note investor receives in the next investment round. Usually, this is the hardest part of the process for founders 🙂 We’ll also break this down so that you can be confident you can do this yourself when raising funds from investors.

SAFE: how does it work and what are the key terms?

A simple agreement for future equity is basically an investor’s subscription to the future shares of the company. SAFE agreements are typically used by early-stage startups that are not yet valued at a level that would make traditional equity investments feasible. Instead, the investor and the company agree on a discount rate or a valuation cap that will be used when the equity is eventually purchased.

Let’s examine how a SAFE works in a simplified way. We’ll take a look at how its key terms work and how to calculate the number of shares that the investor will receive.

Disclaimer: these terms are described in a more complicated way in the agreement itself and we have intentionally simplified it for explanatory purposes here.

There are now a few different types of SAFEs proposed by YC:

- SAFE with a valuation cap and no discount

- SAFE with a discount and no valuation cap

- the MFN SAFE

The first two types of SAFE give away their defining features in their names. The third option, MFN, means that the investor has one chance to upgrade their SAFE to the best conditions proposed by subsequent SAFEs, or if the investor does not upgrade the SAFE, they will receive the same shares of preferred stock as the new money investors in the Equity Financing. You will usually discuss with your investor, which SAFE type works the best for you.

The general idea of working with a SAFE is that you need to input the following numbers:

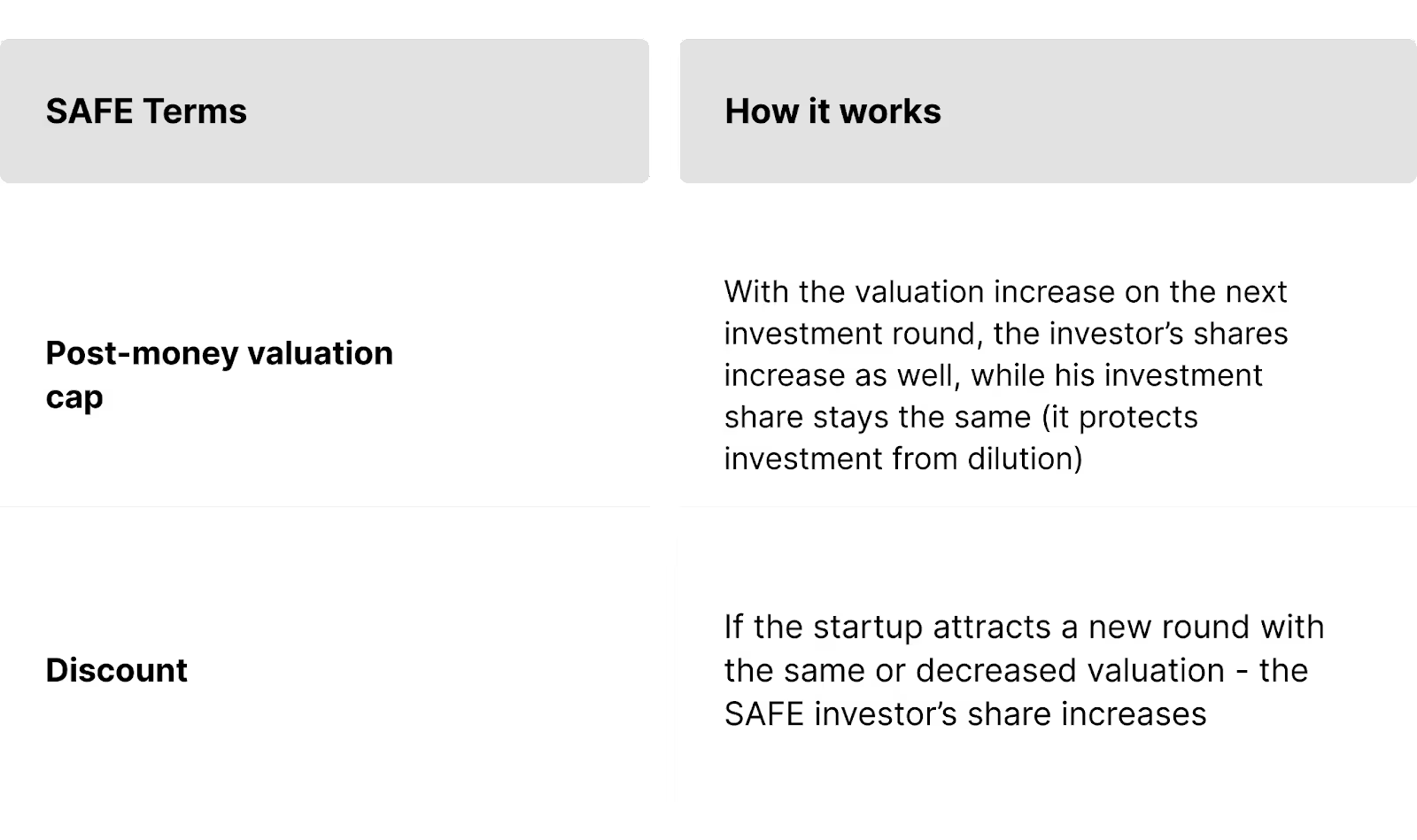

- The post-money valuation cap, which is your company valuation after the investment round, if applicable

- Any discount (if applicable)

- The investment sum

That’s it. This is what makes it really easy to use the SAFE for both founders and investors.

The goal of the SAFE logic is to ensure from the investor’s side that when the startup raises a new round of investments according to a new valuation, investors will receive shares in proportion to what they’ve invested in the pre-seed stage.

For example, if the investor’s check is $200K at a $2m valuation, this gives the investor 10% of shares in the next round. In the next round, if the valuation comes to $5m, the investor will still get 10% of the shares.

If the startup’s valuation has decreased before the next round, the investor will get a higher share in proportion to the valuation decrease.

There are a lot of calculators online that help to work out the number of shares an investor receives via a SAFE, and most of the cap table management tools (like Carta and Ledgy) allow this as well.

📚 NEW! Get help registering a fundraising company

Convertible note: how is it different from a SAFE?

A convertible note is a similar instrument to a SAFE with some slight differences. Like a SAFE, it also works on the principle that investors give money now and receive shares later. But this event of converting investment into shares is defined in the agreement itself.

Contrary to a SAFE, in a convertible note there’s an interest rate and a maturity date in addition to the valuation cap and the investment sum.

If a startup doesn’t attract new investment rounds before the maturity date, an interest rate will apply to the investor’s investment sum. After the maturity date, the investor receives company shares in proportion to their investment plus additional shares accrued as interest.

A convertible loan note also gives an investor an opportunity to claim their investments back with interest after the maturity date if a startup hasn’t raised a new investment round. This is why some founders like this instrument less than Y Combinator’s SAFE. But we need to say that convertible note investors don’t often claim their investments back in practice, and instead this clause serves as an additional reassurance for the investor to protect their investments. Oftentimes, if a startup hasn’t raised a new round before the maturity date, by mutual agreement between the founders and investor, the maturity date will be extended.

💡 Worth checking: Discover tax implications that arise when setting up a US company and setting up a UK company.

Advantages of convertible instruments

Fast and cheap

The beauty of using either a SAFE or a convertible note is that you take a free template document, add a couple of numbers, and it works. It helps tremendously when you want to close a pre-seed round with a dozen angel investors. You don’t need to negotiate the terms with each of them or involve lawyers in negotiations, you only need to agree on the cap, valuation, and sum of the investment.

SAFEs and convertible notes are rather market standard and you do not alter them prior to the signing. Thus, it leads to another obvious advantage of using convertible instruments: you save a lot of money by not engaging legal advisors to prepare customized contracts and supportive documents for each investor. Given that you’re most likely to use these documents for a pre-seed or a seed round, legal fees could take a solid chunk of your investment sum.

More control for founders

Convertible instruments provide founders with more freedom as opposed to investment agreements where investors would expect preferred stock with a board seat, veto rights, and other associated preferences.

“Convertible instruments offer potential benefits for both the investor and the company, such as the ability to convert debt into equity at a later date and providing protection for the investor in case of a down round” - Daria Kurishko, startup legal expert

Disadvantages of convertible instruments

The main thing that makes it harder to work with these instruments is that as a result, you get a complicated cap table (stock ledger).

Convertible instruments are still only 10-15 years old, and despite there being a plethora of online calculators and cap table management tools, some founders still face difficulties with calculating the exact numbers of shares assigned to each investor, advisor, and employee when using a SAFE/convertible note. It is especially complicated if you have several valuation caps and different discounts for different investors, so you need to pay special attention when working with the numbers.

Should this deter you from using convertible instruments for early-stage fundraising? No. Are these limitations something to be aware of? Definitely, yes.

What should I choose: a SAFE or a convertible note?

As we’ve discussed, there’s no real big difference between the two. Perhaps the biggest difference is that a convertible note is a debt instrument with an interest rate.

So it’s really up to you as a founder to decide which route to choose, based on your situation and on your confidence in the instruments available.

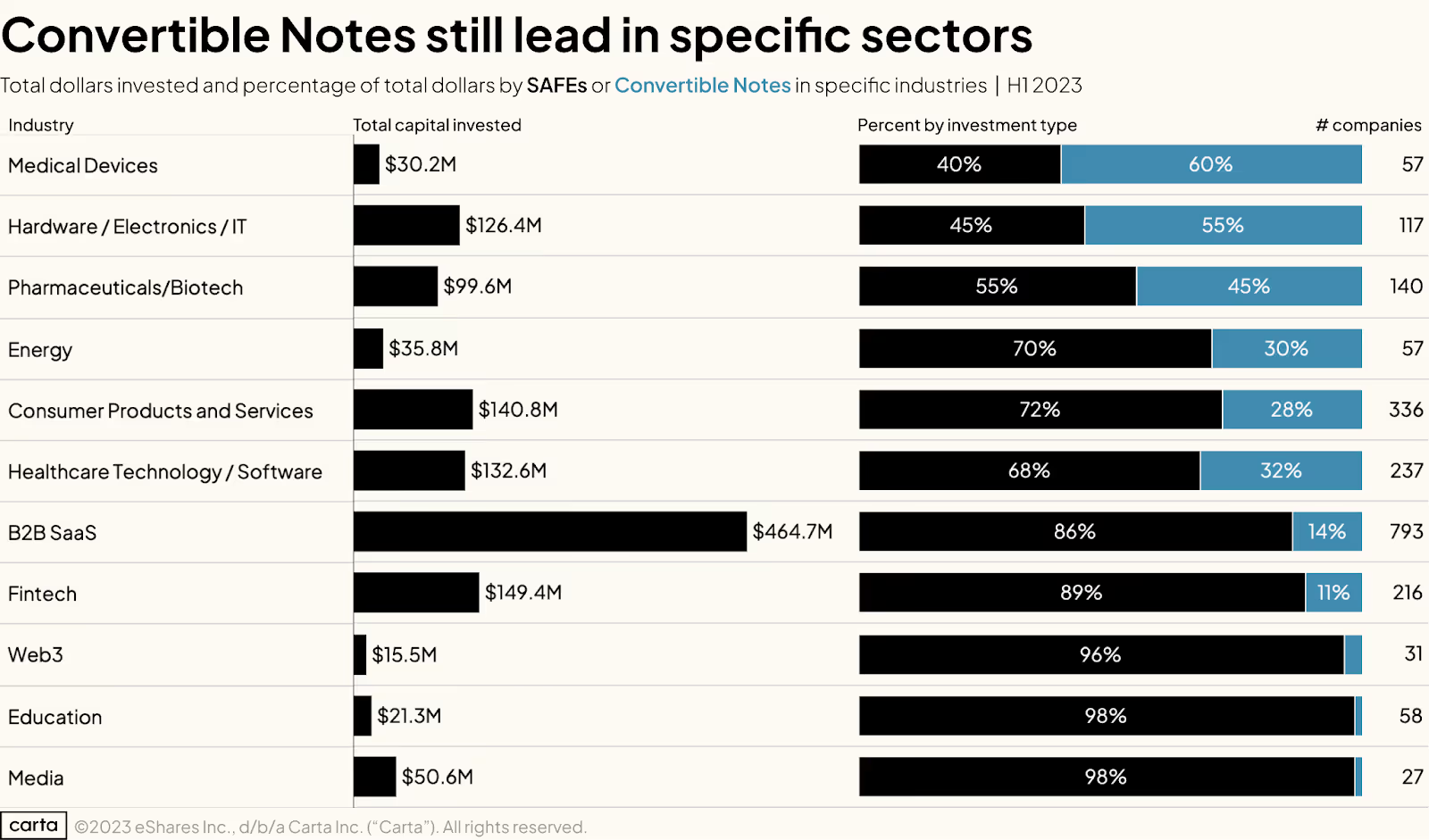

But there’s some data that indicates specific industries prefer convertible notes over SAFEs.

According to the Carta’s State of pre-seed fundraising report, investment through SAFEs accounted for 80% of pre-seed invested capital in Q2 2023. However, certain industries such as Medical Devices, Hardware, and Biotech still see significant investment using Convertible Notes.

It is worth mentioning that companies registered in the US, Canada, the Cayman Islands, and Singapore more commonly use SAFEs as YC proposes specific templates for these jurisdictions.

Investment agreements: how do they work

Investment agreements are a fundraising instrument that are more popular in later rounds. They’re usually used in A+ rounds and they are often signed with VCs, not angel investors. The necessary work to complete the investment agreement starts long before the signing, and usually, VCs and founders have a long relationship-building process that leads to closing a deal. You can check the templates prepared by NVCA or BVCA to see the basic structure. However, most VCs have their own set of templates.

After the first arrangements between the parties are reached, founders and VCs will usually sign a term sheet, which is the first formal step in preparing and signing an investment agreement.

A term sheet is basically a summary of what founders and investors have agreed to verbally during negotiations and serves as a base for preparing future investment agreement documents.

Why is the term sheet important? Although this document is not legally binding, it fixes the main commercial terms and the company's current valuation. It also sets a time frame, during which:

- The VC should conduct the startup’s due diligence

- The VC should prepare all the other necessary documents to complete the investment: shareholders agreement, share purchase or share subscription agreement, updated certificate of incorporation and articles of association/bylaws.

The timeframe set out in the term sheet may vary, but often a period of around 60 days is set, during which the due diligence and agreement preparation should be completed.

If the startup’s valuation has changed during this time, the term sheet may be renegotiated.

📚 Read more: How to approach global compliance when building your startup

What is the document package of the investment agreement?

Signing the equity investment agreement is significantly more complicated than signing just one convertible document. Generally speaking, we can divide all the documents that founders will need to update or prepare into 3 groups:

- Statutory documents of the company: certificate of incorporation, articles of association/bylaws. This is where the share numbers, classes, shareholder’s rights, the rules of the board of directors formation, and other foundational company organization matters are defined.

- Shareholders agreement. This is where you agree with your new shareholders (investors) the terms of entering/leaving the company, good leaver/bad leaver scenarios, the veto right, and other terms. We will go into more detail about this in the next section.

- Share purchase or share subscription agreement. An agreement according to which the investor wires you the sum to your bank account (potentially in several tranches), and you issue them a shares certificate. It includes a timeline, KPIs, conditions precedent to the wire, and warranties and representations provided by the company and the founders.

All these documents need to be updated/prepared after the term sheet is signed and during the time frame agreed in the term sheet.

📚 Read more: How to fundraise for your global business

What are the key terms of an equity investment package and how do they work?

Below we’ll break down the most important terms that founders need to know when negotiating with investors. These terms are reflected in all three document types that we’ve defined above.

Valuation

The company valuation helps founders understand how many shares they should issue to the investor in exchange for the investment amount. The share class is also defined here too. Depending on the round and the investment amount, investors can get shares with or without voting rights, and it can often be preferred stock. This is reflected in the statutory documents.

Option pool

Investors will ask founders to define the option pool in order to motivate early employees and attract advisors with share options. The option pool should be reflected in the agreements and company cap table. Before every new investment round, founders will need to update their option pool to satisfy the startup’s hiring needs. 7-10% are considered to be a market standard.

Vesting

Vesting is an insurance mechanism that lowers the risk of founders leaving the company early with their shares. If there’s a 3-year vesting period for founder’s shares, it means that in a case where a founder leaves the company after 2 years, but on good terms, they can exercise ⅔ of their shares.

Call/put option

A call option is a right that investors reserve for themselves and it gives them an opportunity to make additional investments before the next round happens. A put option allows investors to exercise their right and sell their shares at a predetermined price, effectively limiting their losses.

Pro rata with discounts

This is a term that gives investors the opportunity to keep their share in the company the same during new investment rounds and avoid dilution. For example, if during a new round, an investor’s share drops from 10% to 7.5%, they have a right to purchase the amount of shares that will allow them to keep the 10% stake in the company.

Anti-dilution

This is a term that helps investors avoid dilution if a startup attracts new investments with a lower valuation than in the previous round. With this term effective, a startup would need to issue additional shares to the investor for free in order to keep the investor’s stake the same.

Liquidation preference

This is another term that helps investors protect their investments should a startup make an exit at a lower valuation than on the investment round. In these cases, investors will have a preference to compensate for their loss with the profits from founders' shares at a predetermined coefficient (the industry average is 1x).

Warranties and representations

These are basically assurances made by the parties involved in the agreement regarding certain facts or circumstances. The warranties are usually made by the founders, and they relate to the accuracy and completeness of the information provided about the business. On the other hand, representations are statements made by the parties involved in the agreement regarding their authority to enter into the agreement, the legality of the transaction, and other matters. Both warranties and representations are intended to provide some level of protection for the parties involved in the investment agreement and to ensure that all relevant information is disclosed before the investment is made. It is important to carefully review and understand the warranties and representations included in an investment agreement, as they can have significant legal and financial implications (they might make the valuation and purchase price lower). Results of the due diligence conducted by the VC prior to the signing are usually reflected by the warranties and disclosures.

Founders' covenants and undertakings

These are also affected by the results of the due diligence and problematic issues identified by the investor. If the investor sees some violations, absence of necessary documents, licenses, etc., they might oblige the founders to correct the mistakes prior to receiving the money.

Board of directors

This is what investors demand at later stages of investments - to have at least 1-2 seats in the board of directors, so that they can have influence on the most important decisions in the company. It is important to ensure that the founders are not outnumbered on the board because if the investors control the board, they control the business.

Reserved Matters

This is a list of different business decisions that an investor might have a right to veto. It is important to negotiate that operations in the ordinary course of business are not included here and the company’s business is not affected by the necessity to get investor’s approval on every contract, as this approval sometimes takes time to get.

Informational rights

This term defines the rights of investors to demand certain updates on the company’s metrics, and data, and the frequency and form of such updates.

This is not an exhaustive list. In fact, there are lots more different terms that go into these agreements, but we wanted to focus on some of the most important ones here.

As you can see, investment agreements are very detailed, and a lot more effort goes into drafting and agreeing them from both sides in comparison to convertible agreements.

Advantages of investment agreements

An obvious advantage of this instrument is that it is way more detailed, thus giving founders and investors an opportunity to customize different scenarios to their case. Also, it helps to keep the cap table much more organized making it very clear who receives what amount of shares and when it happens. Additionally, it allows the founders to see what investors they are dealing with. If these investors are qualified and know the market standards then that’s a great sign. Alternatively, they may not be the best match based on continuous heated negotiations and excessive requirements.

Disadvantages of investment agreements

On the other hand, preparing these agreements takes much more time and effort from the founders' side and the legal cost of the preparation is also quite high. Sometimes investors agree to split the legal fees, but often these are paid by founders. In addition to that, investors will receive more rights and this should be carefully considered by founders as they will have much more obligations towards investors compared to when signing a SAFE or a convertible note. Founders should check every provision in favor of the investor if it is market standard and does not provide any unusual preferences that might preclude further rounds or deprive a founder of a shareholding in the company.

📚Read more: How Not to Lose Value in Your Startup Exit Strategy: 10 Best Practices for Founders

Summary: when to use SAFEs, convertible notes and investment agreements

SAFE/Convertible notes → Pre-seed/Seed rounds

Convertible instruments are a popular choice for pre-seed and seed rounds because they allow for flexibility in raising funds and determining the valuation of the company. They also provide a simpler and quicker way to fundraise without having to prepare a complex fundraising package and set a specific valuation for the company at the early stage when it may be difficult to determine its worth. Additionally, convertible instruments offer potential benefits for both the investor and the company, such as the ability to convert debt into equity at a later date and providing protection for the investor in case of a down round.

Investment agreements → Rounds A+

Investment agreements are common for raising funds in Round A and later because they provide a more structured and formalized approach. As the company grows and becomes more established, investors typically want greater clarity and protection around the terms of their investment. The equity investment package outlines the terms of the investment, including the valuation of the company, the ownership percentage that the investor will receive, and additional rights or protections that the investor may have. This can help mitigate potential conflicts or misunderstandings down the line and ensure that both the investor and the company are on the same page. Additionally, investment agreements may provide more favorable terms for investors, such as the ability to participate in future funding rounds or receive priority in the event of a liquidation or sale of the company, etc.

Need to structure your fundraising, but don’t know where to start?

Legal Nodes offers founders a platform to solve their global legal tasks that span multiple countries and areas of law. Preparing for early-stage investing usually involves registering a company (if it hasn’t been done yet or if the existing one doesn’t satisfy investor’s requirements), preparing for due diligence, analyzing the requests of globally spread investors, choosing the right investment documents, analyzing the tax implications of fundraising, and other tasks.

All these questions can be answered and solved via the Legal Nodes platform. With our specially trained Virtual Legal Officers, a network of service providers in 20+ countries, document templates, and a single dashboard to track all your tasks, we’re well-positioned to help busy founders solve complex legal tasks, stay on budget, and keep track of all task progress and communications.

Speak to us to get started, we’ll be glad to help!

This article was prepared by the Legal Nodes team with the contribution of startup legal expert, Daria Kurishko.