In our previous articles, we have discussed different token types and looked into the paid distribution of utility tokens and NFTs. In this article, we shall focus on unpaid token distributions like airdrops, Token Incentive Schemes and others, where a Web3 project issues tokens to tokenholders free of charge.

🏴 Not sure where to begin with the legal tasks for your token distribution? Start here: How to Build a Legal Strategy for a Token Project in 2024

What is an unpaid (free) token distribution?

Token pools comprising a Web3 venture’s Token Cap Table, describe how many tokens are reserved to distribute to a particular group of persons. Some of those pools are allocated for future token distributions that do not require consideration, in other words – payment, to receive tokens. Those token pools include founder, team, advisor, and community pools. Their underlying purpose is to act as tokenized incentives to either attract and retain talent working on the Web3 project or grow and motivate a user base. In this sense, they can easily be compared to share options, rewards, or loyalty schemes used by Web2 companies.

📚 Read more: Models of token distribution and how to legally structure them

Unpaid token distributions amongst founders

It is common for founders of Web3 projects to reserve a percentage of tokens for themselves. Token ownership by founders can be contrasted with founders’ share ownership in Web2 companies.

The transfer of tokens to founders is normally carried out privately with a separate legal instrument, such as a Token Transfer Agreement. This agreement could be later required for financial and tax compliance to confirm the source of funds when depositing the tokens with Web3 custodial services.

Issuing tokens to the team and advisors via Token Incentive Schemes

Web3 founders are competing with the rest of the industry not only for active users but also for the best workers to help them build, scale, and operate their projects. To achieve this, it is common to motivate core teams and advisors with Token Incentive Schemes. Essentially, these schemes function similarly to Web2 Share Option Schemes and Stock Option Plans. A person who provides services or advice to a Web3 business will receive tokens in addition to traditional consideration in fiat or cryptocurrency.

To legalize the issue of tokens to the core team or advisors, Web3 founders need to:

- Prepare and approve a document establishing a Token Incentive Scheme;

- Record the number of tokens allocated for the Token Incentive Scheme in the Token Cap Table;

- Sign employment / freelancer agreement with team members (the type of which depends on their role) or an Advisory Agreement with advisors; and

- Sign a Token Option Agreement with an optionee.

📚 Read more: How to Structure a Token Incentive Scheme and Issue Token Options

What is token vesting and how does it work?

Tokens under schemes are rarely distributed all at once. Instead, they are subject to vesting, which means that they are issued when certain conditions are met. Those conditions can be either one or both of the following:

- The services or advice meets an established KPI. For example, a marketing team member that has attracted a certain number of customers in a given quarter will receive tokens in this quarter. If the KPI is not met, the tokens do not vest; or

- The services or advice is provided over a certain period. This way, the vesting can occur every year, quarter, month, day, week, day, minute, or even every second. For example, if an advisor received tokens with quarterly vesting, each quarter, they will receive more tokens until their Token Option is vested in full. It is also quite common to have a cliff period (normally for one year), where tokens are not vested, but after it is completed, a large portion is allocated at once:

Token vesting can be set up manually or by a smart contract. If the vesting is manual, the information about the vesting schedule and the cliff period are reflected in the Token Option Agreement. If it is set up with a smart contract, it is done fully automatically, so for vesting that takes place every second, it may be that this process is linked to the proof of stake consensus algorithm of a blockchain network, for example.

Key provisions of a Token Option Agreement: “good” and “bad” leavers, token lock-ups

The Token Option Agreement should also contain rules on what happens when the optionee stops providing the services or advice. In this situation, similar to the Web2 Stock Option Agreement, the vesting should stop the day the engagement ends. Additionally, similar to Web2 agreements, the Token Option Agreement could differentiate between “good” and “bad” leavers. Service providers who have left the project due to a violation on their part are normally considered “bad” and are not allowed to keep even the vested tokenholding. On the other hand, “good” leavers retain the portion of token that has already vested but will not receive new tokens after they leave.

It is common that tokens for advisors, as well as tokens distributed to founders, are subject to a token lock-up. A lock-up is a period during which the token cannot be transferred or traded on the secondary market. A lock-up serves as a mechanism to protect the token from plummeting, which could happen when lots of tokenholders sell their tokens at the same time immediately after the distribution. It is common practice to set lock-ups to last from one to two years and it is important that it is enforceable both legally (specified in the public documentation or the private agreement) and technically (included in the smart contract). For tokens issued within Token Incentive Schemes, it could also be part of the document establishing the scheme to which the Token Option Agreement will refer.

Community pool token distribution: airdrops, bounty programs and staking rewards

To attract a larger user base, a certain share of the overall token mass is reserved to be freely distributed amongst the community. The most common marketing technique is user motivation with airdrops. An airdrop is a free distribution of tokens, where they are simply sent to the wallets of active users. Airdrops can be orchestrated in a number of ways and primarily can be divided into two categories; they can be unconditional or conditional. Unconditional airdrops means that tokens are distributed to designated addresses. Alternatively, airdrops can be conditioned to execute when an individual performs a certain action, such as: reposting the project’s post on social media; having a particular balance before an airdrop occurs; or being an active user of the ecosystem and having performed a number of certain actions in the past. A recent example of a conditional airdrop is by Gnosis Safe, where the project distributed tokens to users based on their past contributions and usage.

The latter example is also quite similar to bounty programs. Bounties are tasks, which users can choose to perform to receive tokens. These tasks range from promotional activities such as retweets and commenting, to leaving reviews and even finding bugs in the Web3 project’s infrastructure. Some projects also choose to tie the reward received by users to the impact of the bounty, for example, based on the number of new users attracted by the content created by an existing user in the bounty program.

Another widespread free community distribution is with the use of staking rewards. If the blockchain network underpinning the Web3 project is a proof-of-stake blockchain, tokens could be staked (locked) by the user in a DeFi protocol. In staking, both users and the network win, as staked tokens power up the blockchain network and manage the liquidity of the ecosystem, while also allowing the community to grow their tokenholding. This activity could be compared to how customers who make deposits into a bank allows the bank to give loans and ultimately allows the bank to operate.

Rewards for validators / oracles of a blockchain protocol

The goal of unpaid token distribution to validators and oracles is to reward (incentivize) the main ecosystem participants (contributors) to support the ecosystem and the protocol by approving transactions. These incentives are usually structured in a form of rewards for persons validating transactions within a blockchain protocol (validators) and cross-protocol transactions (oracles).

In other terms, the validators and oracles are rewarded with tokens for creating new blocks with records of transactions they are responsible for.

Can unpaid token distribution still be a “sale”?

Free distribution of tokens is not as simple as giving away promotional codes for Web2 products. In some cases, it can equate to the sale of regulated instruments and be subject to almost the same requirements as “traditional” sales for fiat money.

For example, in the U.S., bounty programs have already been found to constitute the sale of securities. Similar rules could also be applied to airdrops, as stated by the U.S. FinHub. Therefore, when designing token incentive programs involving being promoted publicly, it is important to look at token legal design and make sure that this will not violate financial regulations.

Structuring an unpaid token distribution legally

The existence of consideration for tokens that are distributed does not largely influence where the token issuing company should be incorporated. The more important factor is the legal qualification of the token, as depending on if it’s a utility, security, or governance token will largely decide the jurisdiction for a token issuing company.

Normally, an unpaid token distribution will happen via the following steps:

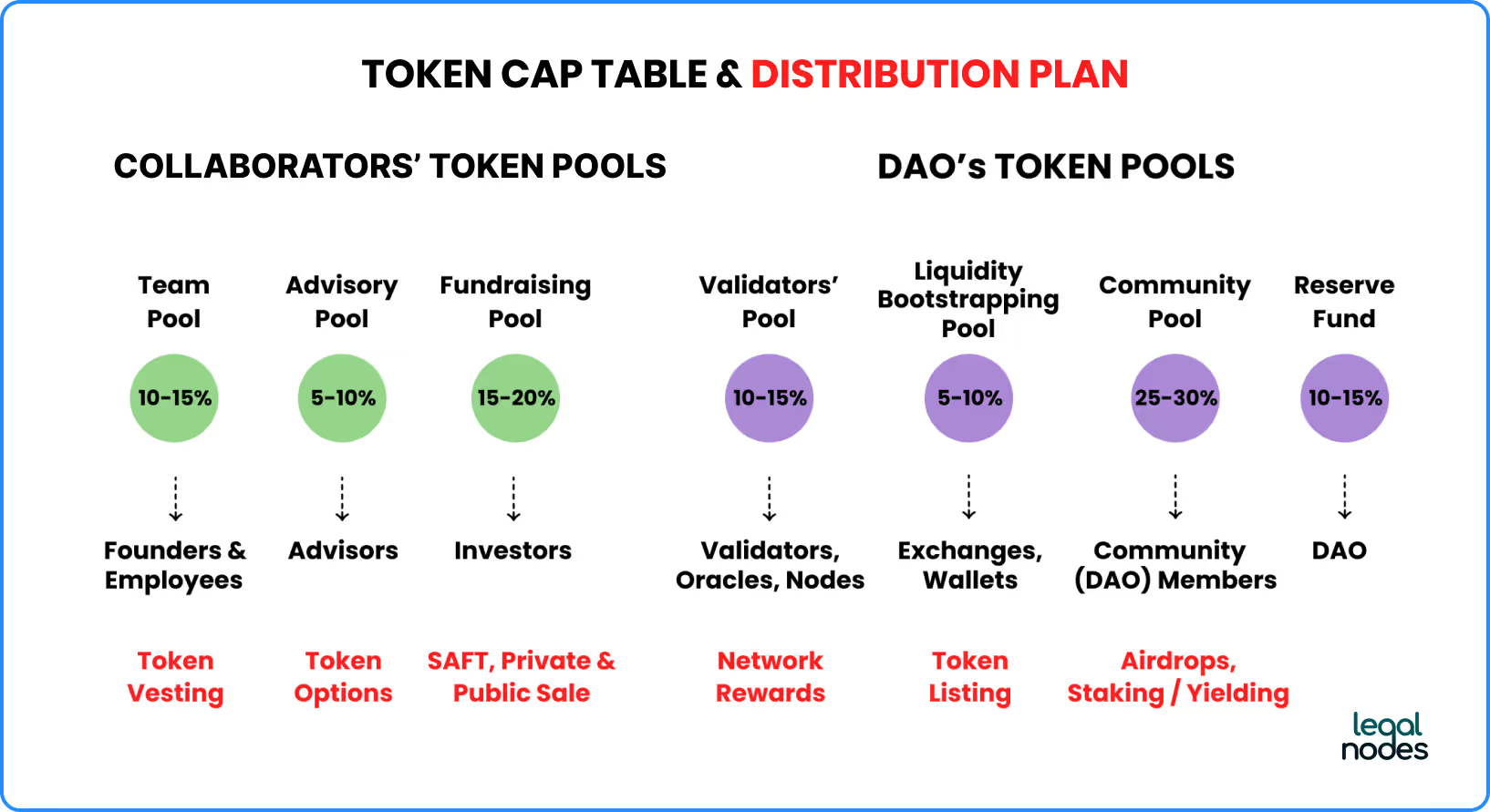

- splitting the tokens into 2 pools: collaborators (founders, advisors, team) and community (DAO Treasury)

- making an unpaid token distribution to the collaborators (team, advisors, investors) from the Token Company;

- making an unpaid token distribution to community by transferring the community token pool from the Token Company to on-chain token Treasury governed by DAO; and

- the DAO will then vote to decide how to distribute the community token pool.

Here’s a visual representation of these four steps, together with the paid distribution of tokens from fundraising pool and liquidity pools:

Depending on the wording of token-specific regulations in some countries, unpaid token distributions may or may not fall under its scope. For example, in the Cayman Islands, the “issuance of virtual assets” is defined as the “sale of newly created virtual assets to the public […] in exchange for fiat currency, other virtual assets or other consideration […]”. Here, the sale is quite clearly understood as receiving tokens for fiat or cryptocurrency, and not in the same way as understood in the U.S. Note, however, that if the tokens are securities, even with a free distribution they would still trigger the securities legislation. On the bright side the issue of utility tokens, whether free or not, would be exempted from all authorization requirements, making a thorough legal analysis an important part of any type of token distribution, whether paid or not.

📚 Read more: How to legally issue tokens in the Cayman Islands

Creating a legal structure for unpaid token distributions

To make sure an unpaid token distribution will not raise any red flags in the investor due diligence process it’s important that Web3 founders:

- Keep records of token pools, distribution channels, and required legal instruments in the Token Cap Table;

- Properly establish a Token Incentive Scheme and sign agreements with each token optionee; and

- Ask a legal professional for a Token Legal Opinion before proceeding with community token campaigns.

Disclaimer: the information in this guide is provided for informational purposes only. You should not construe any such information as legal, tax, investment, trading, financial, or other advice.