The United Kingdom is on the cusp of rolling out a comprehensive regulatory framework for cryptoassets, a move with major implications for Web3 startups.

In the wake of Brexit, the UK is charting its own path separate from the EU’s MiCA regulation – expanding existing financial rules to cover crypto, rather than creating an entirely new regime New rules will introduce licensing requirements for crypto businesses (similar to Virtual Asset Service Provider, or VASP, regimes elsewhere) and clarify the treatment of tokenized real-world assets.

This article provides an overview of the upcoming UK regulations, examines how businesses can adapt, and offers a high-level comparison of the UK’s approach versus MiCA and other popular jurisdictions (Cayman Islands, BVI, Singapore, UAE).

We also include some non-official insights on future legislation and practical advice for startups navigating this evolving landscape.

The New UK Crypto Regulatory Regime (VASP-Style Licensing)

After declaring that “cryptoassets are here to stay,” UK policymakers have been busy crafting a full crypto regulatory framework planned to take effect by 2026.

Rather than start from scratch, the UK is incorporating crypto into its existing financial services regime.

In April 2025, the government published draft legislation (the Financial Services and Markets Act 2000 (Cryptoassets) Order 2025) to formally bring crypto activities into the regulatory perimeter.

Under this approach, new “regulated activities” for crypto are being added to the Financial Services and Markets Act (FSMA) framework, mirroring traditional financial activities but applied to digital assets.

For example, firms will need FCA authorization to

- Operate a crypto trading platform

- Safeguard crypto assets (custody)

- Deal or arrange deals in crypto

- Provide crypto lending or staking services, or issue stablecoins.

In effect, the UK is establishing a licensing regime very similar to a VASP/CASP regime, where any business doing cryptoasset activities in or from the UK (or serving UK customers) must be authorized by the Financial Conduct Authority (FCA).

What does “Qualifying Cryptoasset” mean?

The definition of “qualifying cryptoasset” is broad – essentially any fungible digital token – but it pointedly excludes tokens already regulated as traditional securities or e-money (for instance, tokenized stocks or bank-issued digital money). By doing so, the law avoids double-regulating assets that fall under existing rules, and targets crypto used as investments or payment tokens that currently slip through the cracks.

One notable focus is on stablecoins. The UK’s regime defines “qualifying stablecoins” (cryptocurrencies pegged to fiat currency and backed by reserve assets) as a subset of “qualifying cryptoassets”, and makes issuing or managing stablecoins a regulated activity. This means stablecoin issuers in the UK will be subject to standards on reserve management, redemption rights, and prudential safeguards, akin to what banks or e-money issuers face.

Timeline and status

The UK’s crypto rules are still being finalized as of late 2025. The FCA has been issuing discussion and consultation papers to hash out the details, with final rules expected in 2026. Implementation will likely include an “authorization gateway” opening in 2026 and transitional periods for firms to come into compliance. In the meantime, some interim measures have already kicked in. For example, since October 2023 the UK’s financial promotion rules apply to cryptoassets, meaning any advertisement or solicitation to UK consumers involving crypto must be made or approved by an authorized firm (or a registered crypto firm) and include proper risk warnings. Breaching these promotion rules is a criminal offense, underscoring the regulators’ emphasis on consumer protection even before the full regime goes live.

Additionally, since 2020 the UK has required crypto exchanges and custodians to register under anti-money-laundering (AML) regulations and comply with AML standards – a prerequisite that remains in force. Notably, once the new FSMA authorization regime takes effect, firms that become fully authorized will no longer need a separate AML registration (their FCA license will cover that), although they must still follow the AML rules.

Why does this regulatory approach matter?

The regulatory philosophy behind the UK’s approach is a blend of caution and innovation. The FCA emphasizes “same risk, same regulatory outcome,” seeking to hold crypto businesses to equivalent standards as traditional finance in areas like transparency, operational resilience, and customer care.

However, regulators also recognize the need for proportionality and international competitiveness. In a recent consultation, the FCA even proposed temporarily exempting certain principle-based conduct rules – such as the duty to act with integrity and with due skill, care, and diligence – for crypto trading platform operators in relation to transactions on their platforms. T

his unusual step is meant to let fast-growing crypto firms innovate and compete globally under a slightly more flexible supervisory approach, at least initially. At the same time, the FCA plans to impose stronger requirements in high-risk areas like cybersecurity and operational resilience (prompted by incidents like major exchange hacks). The message is clear: the UK wants to balance innovation with market integrity, leaning into a pragmatic, iterative regulatory process.

Tokenization of Real-World Assets (RWA) under UK Law

Tokenization – the representation of real-world assets (like equity, debt, real estate, or commodities) as digital tokens on a blockchain – is a key frontier in the crypto space.

How will the UK’s legal framework handle these tokenized real-world assets? In general, the approach is to fit them into existing categories. If a token confers traditional rights (for example, a token that represents shares in a company or ownership of a property), it will likely be deemed a “security token”, meaning it’s treated as a specified investment under UK law and regulated just like conventional securities.

Such tokens would trigger all the usual regulations – prospectus requirements for public offerings, disclosure rules, and licensing for intermediaries – just as issuing or trading any security would. In other words, tokenizing an asset doesn’t dodge regulation; it simply moves the asset onto a new technological medium. For instance, a tokenized bond or share in the UK must comply with the Financial Services and Markets Act and the UK Prospectus Regulation if offered to the public or traded on an exchange.

On the other hand, not all tokens of real assets will be automatically caught – it depends on the rights they carry. The UK authorities have stated they intend to avoid regulating tokens that are not used like investments. So if you create a token merely as a voucher or to represent a physical asset for personal use (and it doesn’t confer ownership in a business or debt), it might fall outside the regulatory perimeter. The line can blur, so clarity is expected to improve as the law is tested. For now, startups working on RWA tokenization should seek legal analysis on a case-by-case basis to determine if their token is a security, e-money, a derivative, or another instrument already covered by existing rules.

Beyond fitting tokens into old categories, the UK is actively exploring new frameworks to support tokenization. In 2023, the government enabled the creation of Financial Market Infrastructure (FMI) sandboxes, and by January 2024 the first Digital Securities Sandbox (DSS) was live. This sandbox allows firms (in collaboration with regulators) to experiment with issuing and trading tokenized securities or other financial instruments on distributed ledger technology, under temporary exemptions from certain regulations. The goal is to understand how tokenized markets can operate within a controlled environment and to inform future rulemaking. Similarly, the Bank of England and FCA have been examining how tokenization might modernize clearing and settlement. In a notable speech, a Bank of England official highlighted the potential of RWA tokenization to increase efficiency in financial markets, while cautioning about which asset classes are suitable and the need for sound risk management.

Looking forward, we can speculate that the UK will continue to refine laws to accommodate tokenization. The Law Commission of England and Wales has recommended legal reforms to explicitly recognize digital assets (including tokens) as a distinct form of property under English law. This would solidify token-holders’ property rights and remedies – an important foundation for real-world asset tokens (e.g. making it clearer how ownership of a token relates to ownership of the underlying asset). We may also see tailored regulations or guidance on areas like tokenized funds, real estate tokens, or carbon credit tokens, ensuring they operate with appropriate investor protections but without stifling innovation. In the meantime, UK policymakers tout a “second-mover advantage”: by observing the EU’s and other countries’ experiments with tokenization and crypto markets, the UK can iterate and potentially craft more innovation-friendly rules. For startups in tokenization, the takeaway is to stay engaged with these regulatory developments – and even participate in sandboxes or consultations – to help shape a regime that lets this promising sector flourish.

How Crypto Businesses Can Adapt to the New UK Laws

For Web3 startups and other crypto businesses, the prospect of regulation can seem daunting. However, early preparation and smart compliance strategies will turn this into an opportunity to build customer trust and scale in a sustainable way. Here are some practical steps and considerations for adapting to the UK’s upcoming crypto laws:

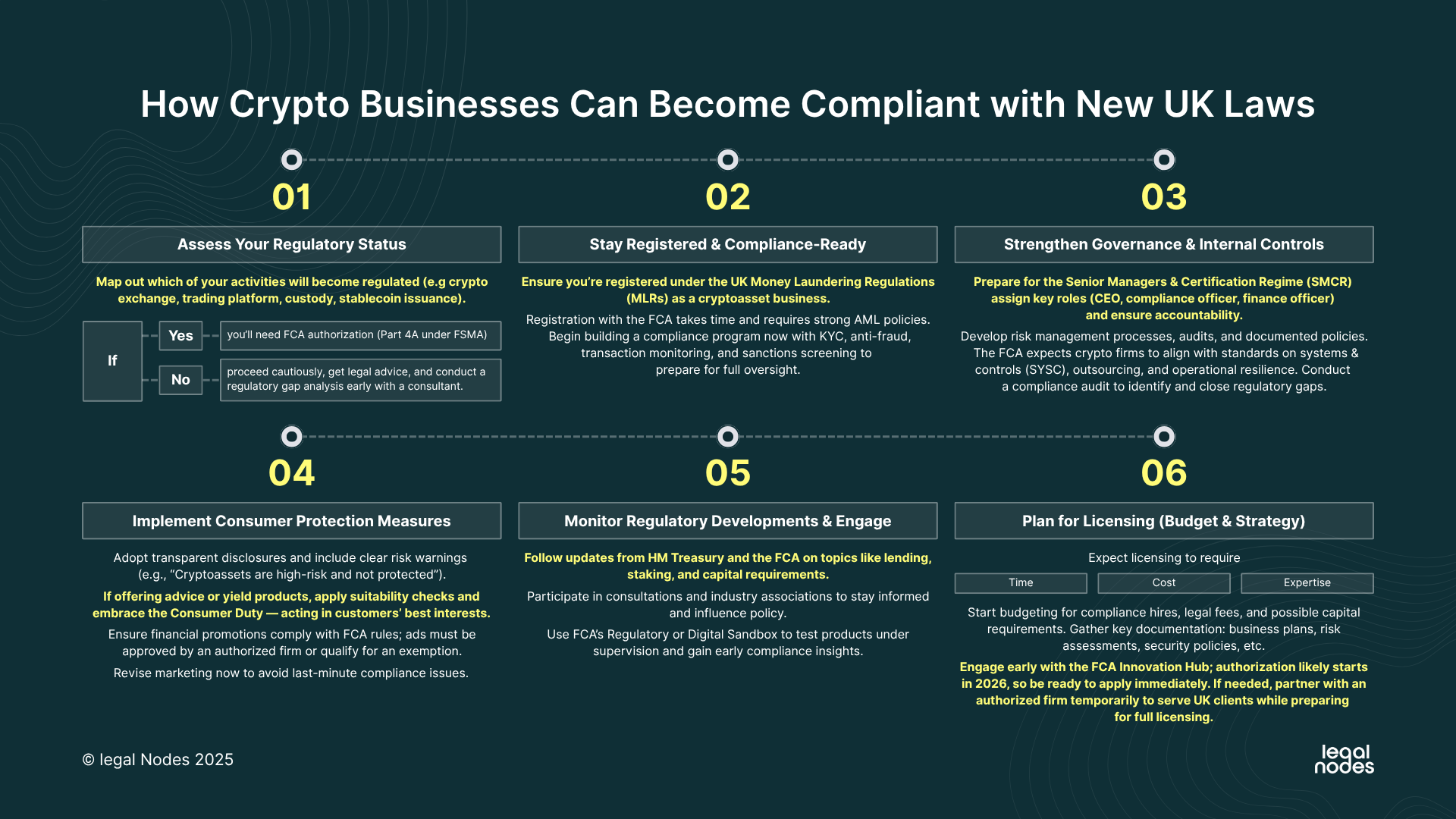

1. Assess Your Regulatory Status

Map out which of your activities will become “regulated activities.” For example, are you operating a crypto exchange or trading platform? Custodying assets for users? Issuing a stablecoin or other tokens to the public? These are all in scope of the new regime. If yes, you will eventually need to obtain FCA authorization (a Part 4A permission under FSMA). If not – for instance, you purely develop software or facilitate peer-to-peer transactions without intermediary control – you might remain outside the perimeter, but proceed cautiously and get legal advice. Early on, engage a legal consultant to perform a “regulatory gap analysis” on your business model.

2. Stay Registered and Compliance-Ready

If you haven’t already, ensure you are registered under the UK Money Laundering Regulations (MLRs) as a cryptoasset business (this is currently mandatory for exchange or custody providers). The registration process with the FCA can take time and requires demonstrating robust AML policies. Even beyond AML, start building a compliance program that anticipates full FCA oversight. This includes implementing know-your-customer (KYC) and anti-fraud measures, transaction monitoring, and sanctions screening, which will be expected as baseline controls.

3. Strengthen Governance and Internal Controls

The FCA has made clear that existing high-level standards will extend to crypto firms. This means startups should prepare to implement the Senior Managers & Certification Regime (SMCR) – identifying key individuals responsible for different aspects of the business and ensuring they are fit and proper. Begin to formalize your governance structure: who will be your CEO, compliance officer, finance officer, etc., and do they have clear roles and accountability? Training senior staff on their duties under SMCR is wise to do early. Likewise, put in place internal controls akin to traditional finance: risk management processes, independent audits or reviews, and documented policies for operations. The FCA’s consultation indicates crypto firms should get ready to comply with rules on systems & controls (SYSC), outsourcing, operational resilience, and more. It’s a good time to conduct a compliance audit internally – identify gaps in your procedures relative to regulatory expectations and start addressing them proactively.

4. Implement Consumer Protection Measures

The UK is pushing a strong consumer protection agenda. By the time you’re authorized, you may need to follow conduct of business rules similar to those for investment firms, covering how you treat retail customers. Startups can get ahead by adopting transparent disclosure practices now. Ensure risk warnings are clear in your app or website (e.g. “Cryptoassets are high-risk and not protected by financial compensation schemes”). If you offer any kind of advice or yield product, consider suitability and appropriateness checks for users. The FCA’s new Consumer Duty – a broad obligation to act in customers’ best interests – is likely to apply in some form to crypto businesses. Embracing this ethos early (for example, by simplifying terms & conditions, and having responsive customer support for dispute resolution) will put you in a good position. Also, remember the current financial promotions rules: if you intend to advertise to UK consumers, ensure you either have someone FCA-authorized to approve the communications or you qualify for an exemption. Many crypto firms have already had to overhaul their marketing materials to comply with these rules – doing so ahead of regulatory enforcement is better than scrambling later.

5. Monitor Regulatory Developments and Engage

The rulemaking process is ongoing. Stay updated with HM Treasury and FCA announcements – for instance, the FCA will release consultation papers on specific topics like crypto lending, staking, and prudential (capital) requirements. Participate in industry consultations if you can; many details (like how DeFi or self-custody might be treated) are still being debated. Joining industry associations or response efforts can give you insight and a voice. The UK regulators have shown willingness to listen to feedback and adjust proposals (e.g. they’ve refined definitions and exclusions after industry input). By engaging, you can help shape rules that make sense for your business model. Additionally, consider utilizing the FCA’s sandbox programs. If you have an innovative product, the Regulatory Sandbox or Digital Sandbox can allow you to test it with regulatory supervision and get early feedback on compliance issues. This can sometimes provide informal relief or guidance that buys you time to fine-tune before the full regulations hit.

6. Plan for Licensing (Budget and Strategy)

Obtaining a license will require time, expertise, and money. Start budgeting for increased compliance costs – this might include hiring compliance officers or legal counsel, investing in regulated infrastructure (like custody solutions that meet security standards), and setting aside regulatory capital if required (the FCA is considering capital requirements for certain crypto firms similar to those for financial institutions). Begin gathering documentation that will be needed for a license application: business plans, risk assessments, security policies, etc. It’s wise to engage with the FCA early if possible – for instance, via their Innovation Hub or preliminary meetings – to discuss your path to authorization. Firms likely will not be able to apply for authorization until 2026, once rules are final. But that first application window will become crowded; being prepared means you can submit a strong application on day one, minimizing delays. In the interim, if you’re serving UK customers, ensure you have any necessary temporary permissions or exemptions to operate. And if the compliance burden seems too high for your startup’s current stage, you may consider partnering with an authorized firm (for example, using an authorized e-money institution for custody or payments) to bridge the gap until you can get your own license.

In summary, don’t wait for the law to hit – start behaving like a regulated firm now. Many best practices (robust security, honest marketing, prudent financial operations) not only prepare you for regulation but also make your business more trustworthy to users and investors. Adapting to regulation is definitely a challenge for startups, but those that do so will likely have a competitive edge as the industry matures.