Fractional Real Estate Ownership in the UAE: Tokenization, Crowdfunding and REIT Models

Introduction – Three Models for Fractional Investment

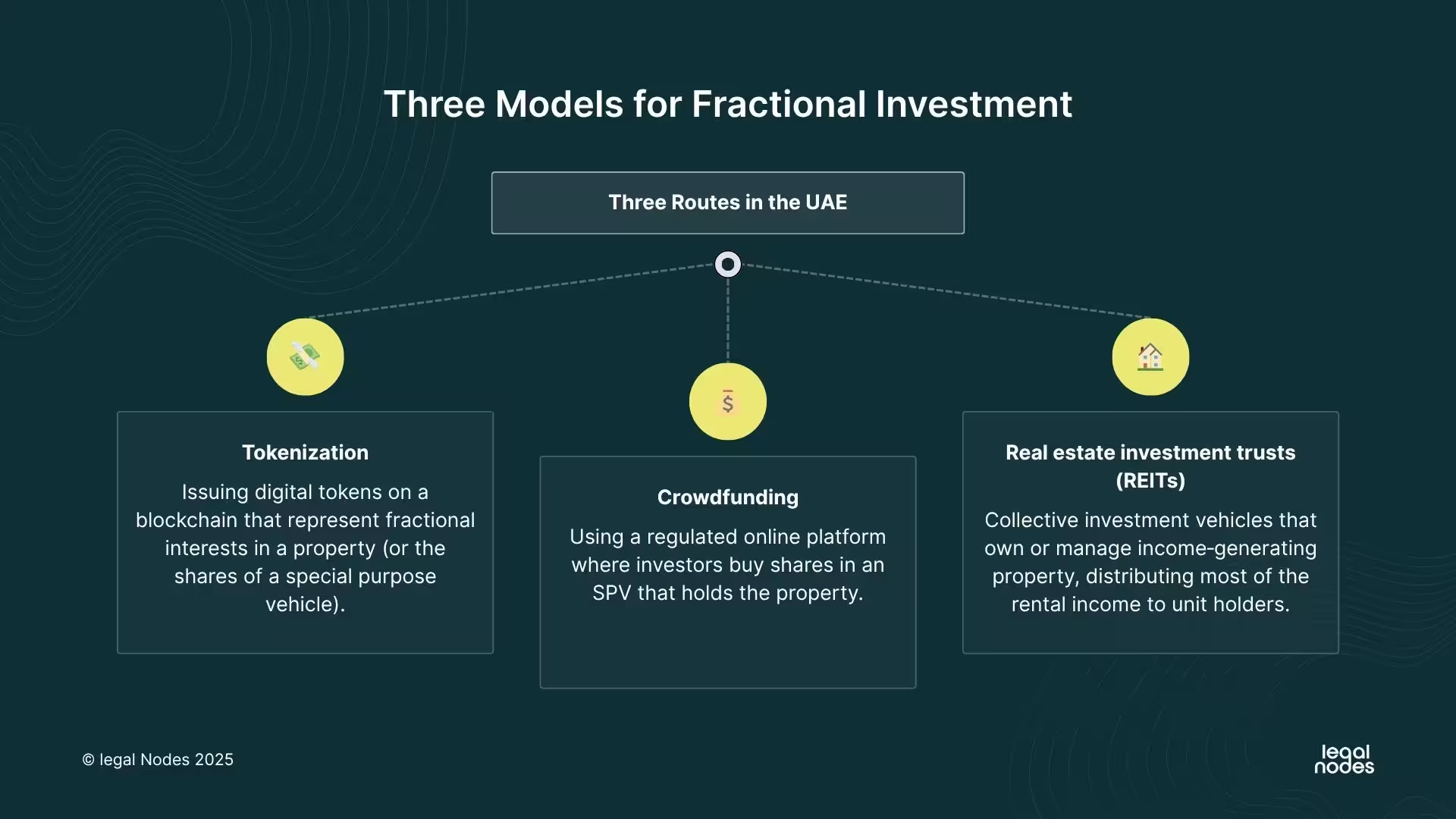

Fractional ownership of real estate allows multiple investors to share the benefits of a property without needing to buy it outright. In the UAE, Web3 start‑ups looking to democratise property investment have three main approaches:

- Tokenization – issuing digital tokens on a blockchain that represent fractional interests in a property (or the shares of a special purpose vehicle).

- Crowdfunding – using a regulated online platform where investors buy shares in an SPV that holds the property.

- Real estate investment trusts (REITs) – collective investment vehicles that own or manage income‑generating property, distributing most of the rental income to unit holders.

Other structures such as traditional property funds and co‑ownership exist, but tokenization, crowdfunding and REITs are particularly relevant to FinTech and Web3 founders.

They offer ways to raise capital from a broad investor base while complying with local regulations.

The sections below describe each model’s nature, licensing options in the UAE’s major jurisdictions (Dubai mainland/VARA, Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC)), the key regulatory requirements and costs, their advantages and drawbacks.

Tokenization Route

Nature of the Model

Tokenized real estate converts ownership or economic rights in a property into digital tokens recorded on a blockchain.

Each token represents a fractional share in the underlying asset and may convey rights such as income or voting.

Smart contracts automate investor onboarding, transfers and rent distributions, making transactions faster and potentially cheaper.

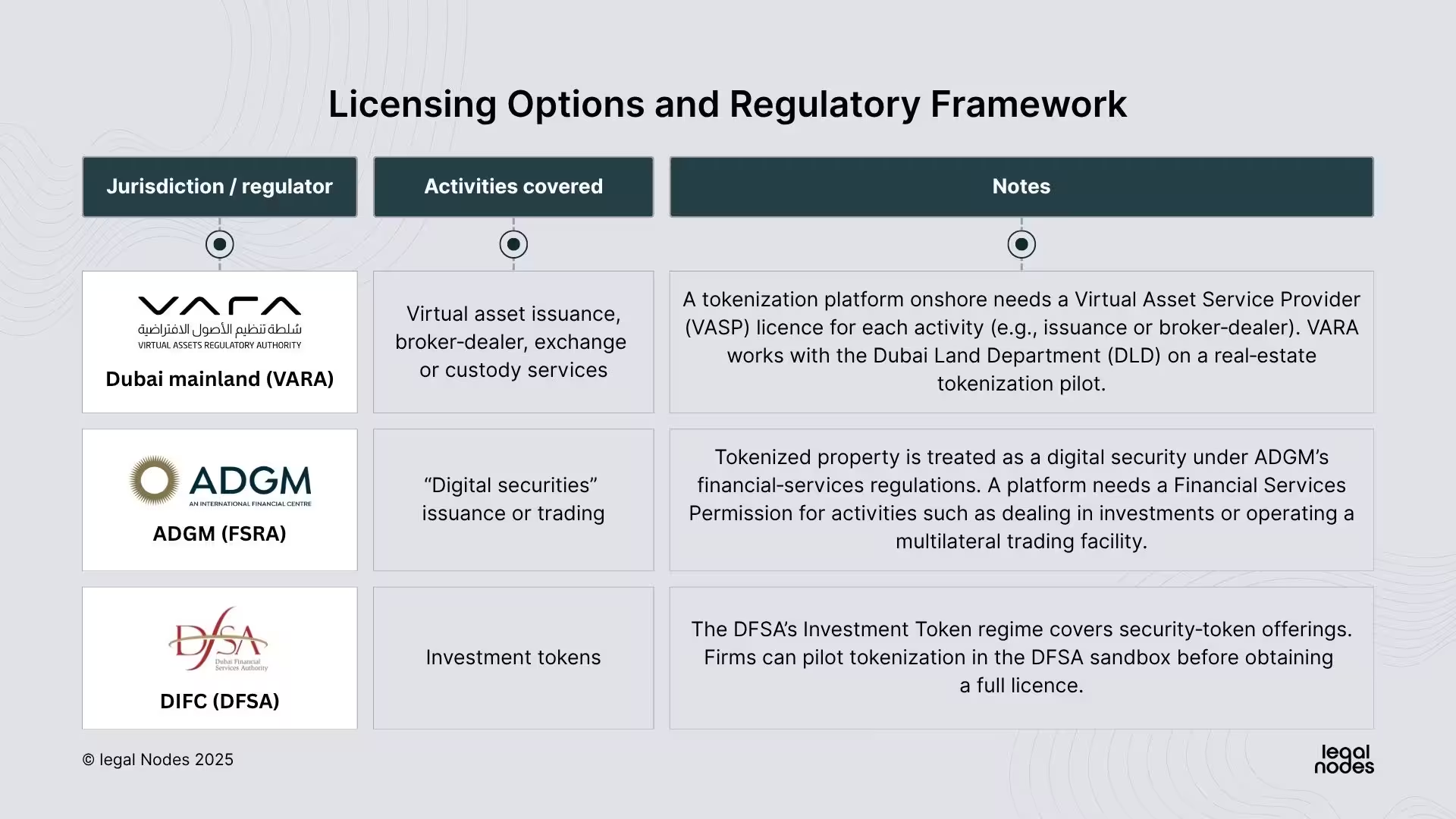

Because tokenized property typically confers real ownership & investment income, UAE regulators treat these tokens as securities, meaning securities laws and investor‑protection rules apply.

Licensing Options and Regulatory Framework

Key Requirements and Licensing Costs

- Entity and Substance: The company must be incorporated in the chosen jurisdiction and maintain a physical office. Senior management and compliance officers must reside in the UAE. Management must pass fit‑and‑proper tests, often requiring 5–10 years’ relevant experience.

- Capital and fees: Tokenization is the most capital‑intensive route. DFSA guidance indicates a base capital around USD 140,000 for platforms that deal in investments, and ADGM often expects USD 250,000 or more for similar activities. Application and annual supervision/license renewal fees are substantial (e.g., VARA’s AED 100,000 application and AED 200,000 annual fee per regulated activity).

- Compliance controls: Detailed anti‑money‑laundering (AML) and know‑your‑customer (KYC) procedures are required. Regulators also require cybersecurity audits, business‑continuity planning and custody arrangements. Investment marketing materials may need prior approval, and retail participation is often limited to professional investors or specific testing regimes.

Pros

- Global reach and liquidity: Digital tokens can potentially be traded worldwide, bringing stock‑like liquidity to real estate.

- Automation and efficiency: Smart contracts facilitate near‑instant settlement and rent distribution, reducing intermediaries and transaction costs.

- Transparency: Blockchain records create an immutable audit trail, enhancing trust and reducing fraud risk.

- Innovation: Tokenization aligns with broader Web3 and DeFi trends, enabling novel structures such as different token tranches.

Cons

- Regulatory complexity: Multiple regulators (VARA, DLD, SCA) may be involved, and the rules are evolving. Missteps can result in enforcement actions.

- High costs: Licensing fees and capital requirements can exceed those of crowdfunding or REIT managers; VARA fees alone can be hundreds of thousands of dirhams per year.

- Technology risks: Smart‑contract bugs, wallet hacks and custody issues introduce new points of failure.

- Market adoption: Secondary markets for security tokens remain nascent; investors may face limited liquidity in practice.

Crowdfunding Route

Nature of the Model

Real‑estate crowdfunding uses an online platform to raise capital from many investors. Each property is typically held in a Special Purpose Vehicle (SPV) and investors buy shares in the SPV, entitling them to rental income and a share of capital appreciation. Platforms such as SmartCrowd and Stake operate under this model and are licensed by the DFSA. Crowdfunding relies on conventional shares rather than blockchain tokens.

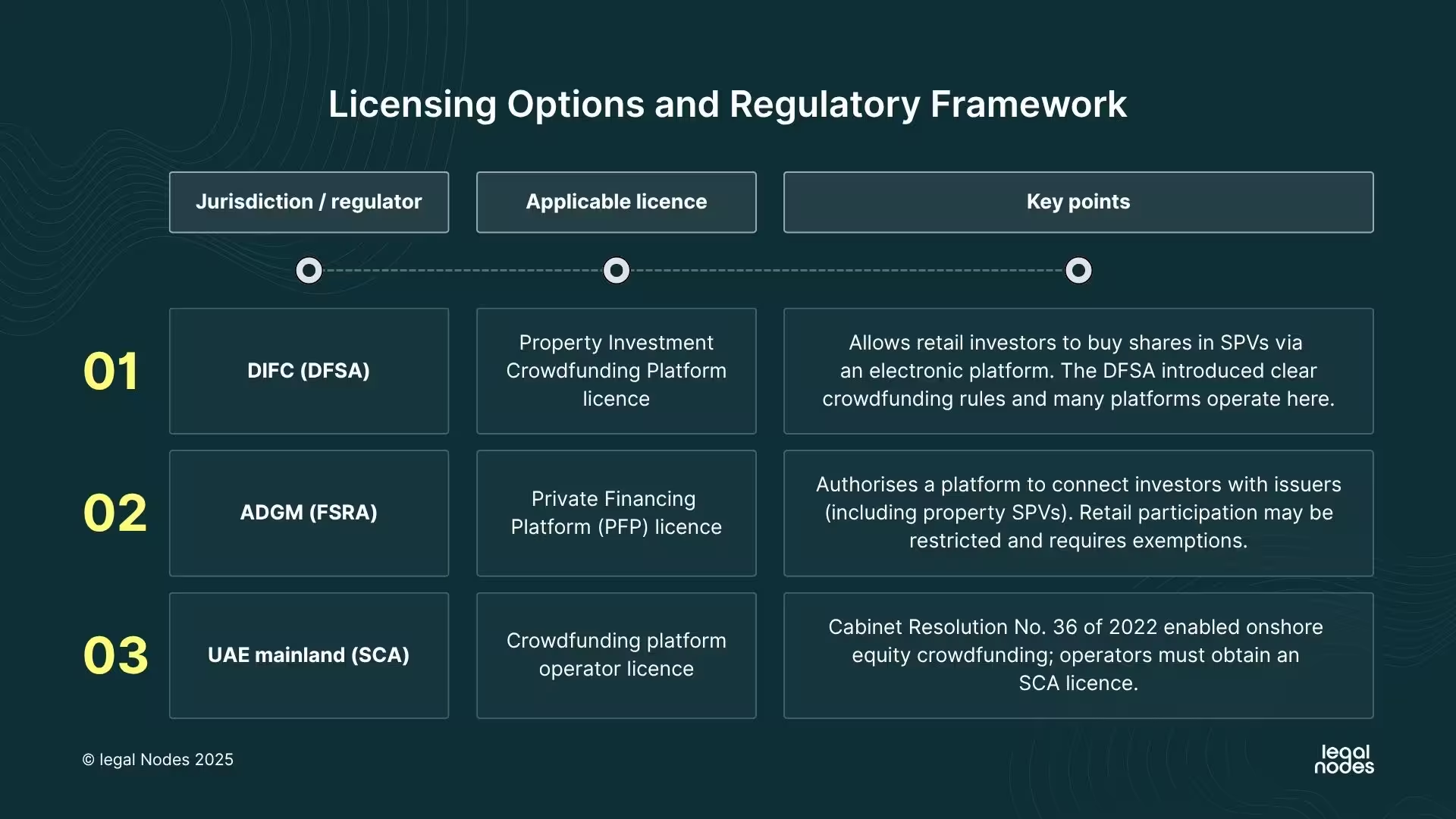

Licensing Options and Regulatory Framework

Key Requirements and Licensing Costs

- Incorporation and leadership: Platforms must be incorporated in the jurisdiction and have a local office. Approved individuals (Senior Executive Officer, Compliance Officer, Finance Officer) must meet experience and fit‑and‑proper criteria.

- Capital requirements: DFSA requires USD 140,000 base capital for crowdfunding platforms. ADGM’s initial capital may start around USD 10,000 but often needs USD 250,000 for a viable business. The SCA requires at least AED 1 million paid‑up capital for crowdfunding operators.

- Fees: Application fees are modest compared with tokenization. DFSA license costs roughly USD 5,000 to apply and USD 10,000 annually. An additional USD 20,000 is required if the platform will deal with retail clients. SCA fees include a licence fee and possibly an annual renewal; there may also be a percentage fee per offering. FSRA (ADGM) charges USD 10,000 for the regulated activity of operating a private financing platform; an extra USD 10,000 is payable for each additional regulated activity.

- Operational controls: Platforms must maintain separate client accounts, perform AML/KYC checks and provide robust IT systems. Retail investor limits apply – e.g., DFSA‑regulated platforms cap individual investment per property and overall holdings. Regular reporting to the regulator and audited financial statements are mandatory.

Pros

- Regulatory clarity and trust: Crowdfunding frameworks in DIFC and ADGM are well established, giving investors confidence and providing a structured path for compliance.

- Access to retail investors: Platforms can accept small investments from the general public, widening the investor base. Minimum investments can be a few hundred dirhams, democratising property investment.

- Lower cost and complexity: Capital and fees are lower than tokenization; no blockchain development is required. Start‑ups can launch relatively quickly via regulatory sandboxes.

- Proven model: Existing platforms demonstrate market demand and provide case studies for operations, partnerships and customer education.

Cons

- Limited liquidity: Investors generally hold their shares until the property is sold; secondary markets are limited compared with tokenized tokens.

- Investment caps: Regulators restrict how much each retail investor can invest in a single project, meaning large funding rounds require many small investors.

- Operational burden: Managing hundreds of retail investors per property requires robust back‑office systems and investor communications.

- Less innovative: Crowdfunding does not leverage blockchain or DeFi, which may lessen its appeal to tech‑savvy investors.

Real Estate Investment Trust (REIT) Route

Nature of the Model

A real estate investment trust is a collective investment vehicle that pools money to invest in income‑producing property, distributing most of its net income to unit holders. REITs pool multiple properties, providing regular dividend distributions and diversification across assets. Investors buy units in the REIT, which may be publicly traded or privately placed. REITs provide exposure to diversified portfolios (commercial buildings, residential complexes, logistics assets) and are run by professional fund managers. In the UAE, REITs exist both onshore (regulated by the Securities and Commodities Authority – SCA) and in the financial free zones (regulated by the DFSA in DIFC and the FSRA in ADGM). Dubai’s 2022 REIT Decree introduced privileges for REITs that hold at least AED 180 million of real estate and register with the Dubai Land Department. The REIT must also engage licensed fund managers, independent custodians/trustees, auditors and property valuers.

Licensing Options and Regulatory Framework

Pros

- Stable income and diversification: REITs pool multiple properties, providing across assets. Listed REIT units can be traded on exchanges, offering more liquidity than private property holdings.

- Regulatory credibility: REITs operate under well-developed investment fund frameworks in DIFC, ADGM and onshore, providing investor protections and clear governance.

- Tax efficiency and privileges: UAE REITs benefit from favorable tax treatment (dividends may be exempt from corporate tax) and, in Dubai, reduced real-estate registration fees (2 % on acquisitions).

- Access to institutional investors: Because REITs are established under investment-fund laws, they can attract institutional investors and list on recognized stock exchanges like NASDAQ Dubai, increasing fund-raising potential.

Cons

- High setup and compliance costs: Establishing a REIT requires fund‑management infrastructure, independent trustees and auditors, and significant capital. Manager licenses and fund registration fees can amount to tens or hundreds of thousands of dollars.

- Regulatory constraints on leverage and development: Borrowing and development caps (70 % and 30 %) limit risk but may reduce potential returns【219†L143-L145】.

- Minimum asset size: Dubai’s REIT Decree demands at least AED 180 million in real estate to access privileges【119†L60-L66】, making REITs suitable for larger portfolios rather than single assets.

- Less flexibility: REITs must distribute most of their income and cannot easily retain earnings for growth; they are also subject to mandatory dividend policies and periodic valuations.

Conclusion – Choosing the Right Model

Tokenization, crowdfunding and REIT structures each enable fractional real‑estate investment but suit different business strategies:

- Tokenization is ideal for Web3‑native platforms aiming to tap into global crypto capital and offer secondary trading of fractional units. It demands significant capital, specialist technology and navigating evolving virtual‑asset regulations, but it positions at the cutting edge of PropTech.

- Crowdfunding is a pragmatic choice for start‑ups wanting to launch quickly with lower capital outlays. It offers broad retail access through regulated online platforms and aligns well with small‑ticket investors. Limited liquidity and investor caps, however, mean returns depend on the asset’s long‑term performance.

- REITs are best suited to larger portfolios seeking stable income and institutional investors. They provide legal certainty, exchange‑listing potential and Dubai‑specific privileges (reduced real‑estate fees and foreign ownership flexibility), but they require substantial assets, professional fund management and adherence to strict distribution and leverage limits.

There is no “one‑size‑fits‑all” model.

The founders should assess their target investors, funding capacity, technology capabilities and risk appetite when choosing between tokenization, crowdfunding and REIT structures. In some cases, a hybrid approach may emerge; for example, a crowdfunding platform could later tokenize SPV shares, or a tokenization company might evolve into a REIT manager once it amasses sufficient assets.

The UAE’s regulatory environment continues to evolve, and the authorities have signaled support for innovative fractional‑ownership models that broaden investment opportunities while safeguarding investors.